Battery energy storage is now a thing. No caveats needed.

Sometimes we talk about a new thing for a long time, then are disappointed when that thing never seems to happen. Then we wonder if it will ever happen, because we are impatient people. Gartner captured this phenomena with its hype cycle, where technologies like VR/AR and crypto remain firmly on the left (Magic Leap anyone?). Battery energy storage for the grid has been one of these things. The idea that batteries can replace gas plants with energy stored from excess clean generation has always sounded like a winner. Yet deployment of battery-based storage has been incredibly slow going. Until now, that is. Battery storage is now a thing, and if you weren’t paying attention in the last year, you may not have noticed. So let’s catch up on battery energy storage in February 2022.

Grid storage in California (aka seeing into the future)

It’s often repeated that if you want to see into the energy future, look at California. Last month, PG&E revealed plans for 1.6 GW of new grid attached battery storage, bringing its total storage capacity to 3.3 GW when it comes online in 2024. PG&E’s proposal is in response to a CPUC order last year to bring 11.5 GW of clean resources online by 2026, an order that only came about after a previous plan that included new gas generation was questioned by groups such as the Union of Concerned Scientists. An energy analyst with the org explained,

"...recent [integrated resource planning] analysis and modeling hasn’t shown any need for fossil fuel resource procurement. We already have tens of thousands of megawatts of gas capacity on the grid, and there’s really no evidence that we need additional insurance in the form of fossil fuel resource procurement.”

That’s right. Most studies agree that California doesn’t need any new fossil-based generation to meet future energy needs. The first joint agency report from California’s SB 100, which mandates 100% carbon-free energy by 2045, lays out a future where we triple our current electricity demand, and meet that need through clean energy generation and storage. The report estimates California needs about 50 GW of battery capacity in total.

How does the CPUC’s 11.5 GW order compare to California’s current capacity? In 2021, California had 13.8 GW of utility solar and 31 GW of gas capacity. So 11.5 GW is a meaningful amount of storage, and given a few favorable developments, we could easily see more come online more quickly and in greater quantities than anticipated.

Meanwhile, Across the US

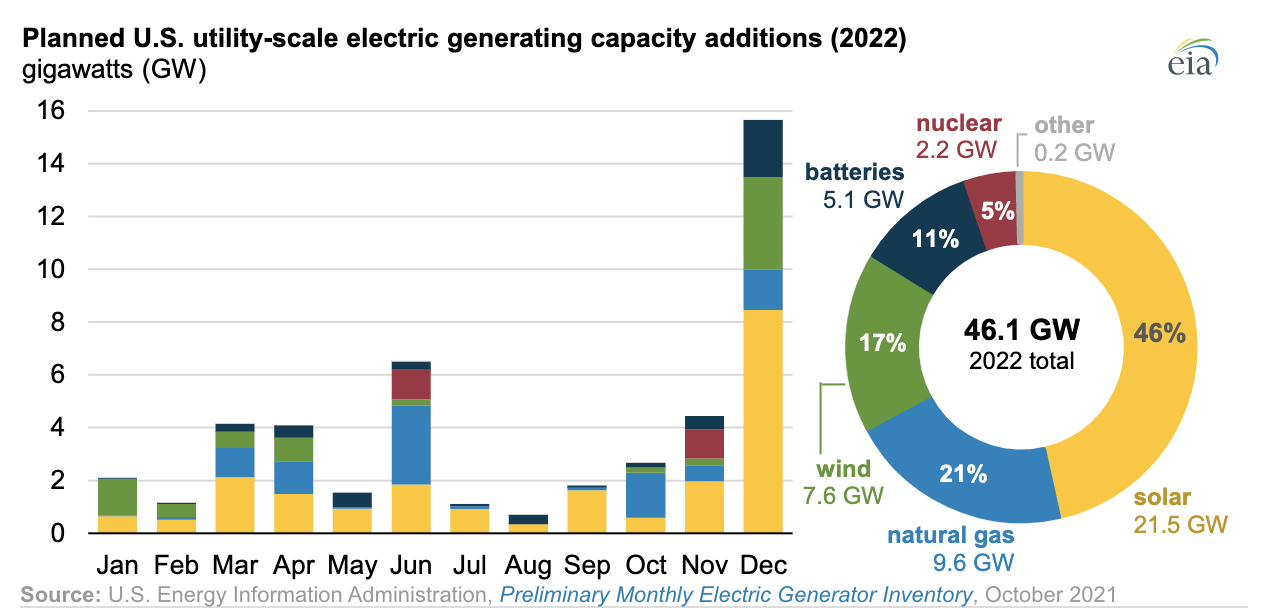

To put California’s new storage projects in perspective, the US had less than 1 GW of grid-attached battery storage at the end of 2020, and only 6 GW at the end of 2021 (SPD Global). The EIA anticipates we should about double that capacity this year with the addition of 5.1 GW more batteries planned:

Batteries make up 11% of expected 2022 US capacity additions. It’s worth emphasizing again that we plan to add about the same battery capacity this year as we have in all previous years.

Not all that capacity will be mega-sized projects either. The Wall Street Journal recently ran a piece on energy storage in New York featuring NineDot, a developer that is putting battery storage in and around New York City. One of the sites is being co-developed with Fermata, a fleet management and bi-directional EV charging solution. New York state is targeting 6 GW of storage by 2030, from only 130 MW operational today.

These numbers are meaningful in that they demonstrate storage is establishing a foothold where it had none just two years ago. The ramp is yet to come however. Research by NREL projects the US should install between 200 GW - 930 GW of grid-attached storage across the country by 2050, depending on the generation mix and future costs. So yeah, we’re going to be attaching many more batteries to the grid.

Why more gas?

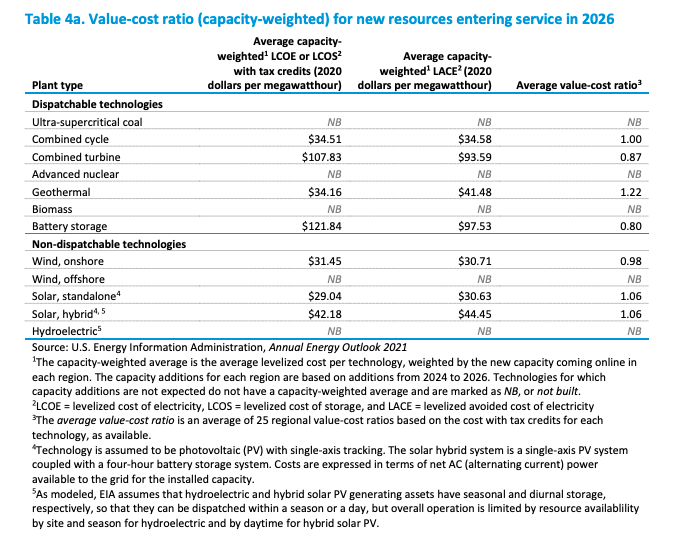

21% of the EIA’s expected capacity additions for 2022 is gas generation. Why are we still building gas plants at all? Of course project economics plays a role, but it isn’t the whole story. In its 2021 energy outlook, the EIA projected the net economic value of generation resources built in 2026 (higher value-cost ratio is better), and natural gas generators are indeed more economically positive than standalone battery systems.

But solar and solar-battery hybrids beat gas on economic value in most regions, so economics is not always the deciding factor. Instead it’s geographic constraints, experience, and risk. In Glendale, CA, without the space to add a solar plant, and constrained transmission lines that add risk to importing solar from a different location, Glendale’s planners prefer to upgrade their existing gas plant rather than take on risk with a fully clean portfolio. In constrained areas like Glendale, gas plants are justified as insurance, a hedge or a de-risking choice to locate generation within city boundaries.

This dynamic plays out at a larger scale at the state and grid operator levels. As the economic case for solar and solar hybrid over gas becomes more undeniable, it’s down to nuts and bolts constraints like geography, operator experience and the quickly evolving standards and tools that are used to value the capacity contributions of intermittent resources, so that the “new” approaches are de-risked and planners ensure they can deliver the energy reliability the public expects. Even in a progressive energy environment like California, to achieve results such as the roadmap to 100% clean energy in LA by 2035 requires a level of coordination and cooperation across operators, distribution utilities, developers and local governments that we haven’t seen in a generation or more. That can only happen with sustained public support – it’s up to us to keep it going.

Hybrids (not vehicles) take over

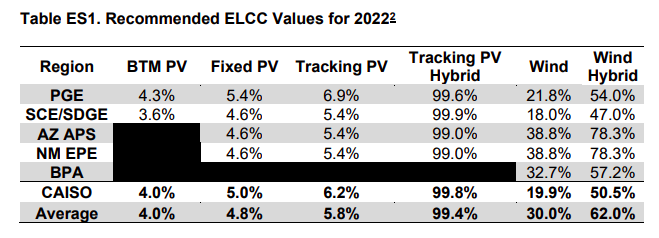

While grid-attached energy storage can be developed as either standalone systems or hybrid (co-located with solar or other generation), the latter offers a strong economic incentive in the form of the federal Incentive Tax Credit (ITC), which can be applied across the whole cost of a solar/battery hybrid system, as long as the battery charges with clean energy. Hybrid systems also gain value vs standalone systems for their capacity value for resource adequacy. While regions such as the Midwest with low solar penetration value new standalone solar capacity up to 50% of its nameplate value, California values new solar capacity at only 4-6% of its rated value, dropping to under 2% by 2030. On the other hand, hybrid systems are valued at 99.8% today and only drop to 93.2% by 2030.

Today new solar developments in areas of high solar penetration (e.g. the West) mostly incorporate battery storage – close to 90% of solar projects in the CAISO interconnect queue at the end of 2020 included paired storage, as did 67% of the other projects in the West region. This pattern will repeat in other regions as the country adds more new solar capacity than all other types of generation combined.

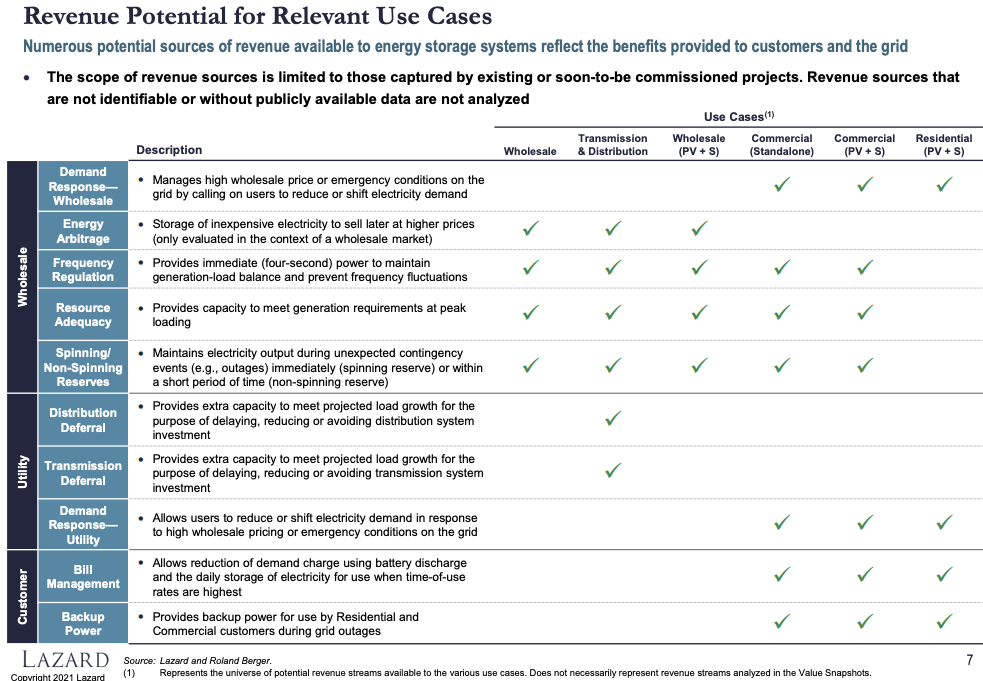

Managing storage value

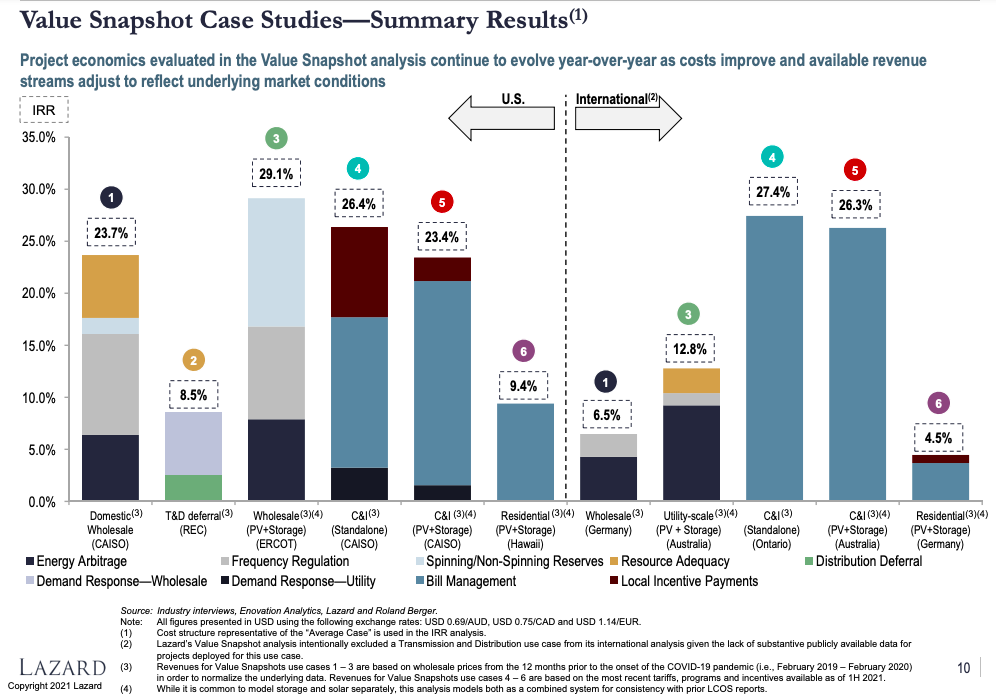

How do storage developers and operators make money? Lazard lays out the use cases and profiles a few actual projects in its Levelized Cost of Storage analysis.

And here are some actual results that show IRR’s between 9% and 29% in the US depending on region and use cases.

Add on top of this revenue the cost to deploy these batteries and the cost of software to manage them and you have revenue models of companies like Stem and Fluence. Stem is a US leader in energy storage management for commercial clients and cites 1.4 GWh of storage capacity under management as of September 2021. Fluence projects 2.7 GW of storage and renewable assets under management by the end of 2021, up from 232 MW the year before.

In California, new clarifications governing the treatment and market participation of hybrid systems provided a more sound economic basis for financiers and developers. But a debate continues about the participation of hybrid resources in resource adequacy requirements, i.e. must hybrid resources be available to discharge at all times or can they participate at the manager’s discretion? Today those hybrid resources are exempt, meaning they are not required to participate in markets. That is likely to change as the role and performance of hybrid systems becomes clearer with operating experience.

Behind behind-the-meter (BTM) AKA on-site storage

The CA wildfires in 2019 were a turning point for attaching battery storage to new residential solar. I heard that battery attachment rates went from less than 30% to 100% over that period. As someone who experienced the triple whammy of staying indoors for air quality, schools and public gathering places shut because of COVID, and PG&E’s preventative power shutoffs, I can attest to the appeal of a home backup energy system. It remains to be seen whether this effect will persist – consumers can have short memories for rare events. For what it’s worth, Sunrun expects a battery sales increase of 100% in 2021 over 2020.

The topic of distributed storage is explored in detail in a recent report from LBNL. A homeowner with time-of-use rates (uncommon) can make an economic case to justify home batteries simply for peak hour energy supply. But reliability and emergency supply is the value to homeowners that may be a more compelling driver of installations, with the subsequent ways to monetize the battery viewed as a nice cost reduction tactic. In other words, we install batteries for security and comfort, not to make money.

The report also highlighted the value of FERC 2222, issued in 2020, which enabled aggregations of distributed resources (DER) to participate in wholesale markets, unlocking new economic possibilities for distributed energy. That means rooftop and community solar, demand response, hydrogen fuel cells, battery storage, electric vehicles and microgrids can now be treated as generation assets like traditional generators by system operators and planners. There is still work to do in clarifying how participation looks in each of the regional markets – some aggregators find the locational and scale requirements overly restrictive, effectively locking out many of the participants that this order aimed to encourage. On the other hand, Duke Energy in Florida just announced a new “Bring Your Own Battery” program to explore the potential of a Virtual Power Plant (VPP) to meet peak demand needs. Also see how Sunrun and Ford are working together to support the F150 Lightning’s integration into home electrical systems.

In the commercial market, 24/7 clean energy may be a catalyst and accelerator for energy storage. With corporate and industrial clients increasingly interested in procuring clean energy that matches their hourly needs, and avoiding demand charges levied by distribution utilities, companies like Stem and Alight Energy are increasingly called upon for energy storage.

Today distributed energy is more expensive than utility-scale energy on a per kWh basis, but people and organizations want control, and less reliance on the grid. As utility rate structures evolve to better reflect value, costs decline as we scale battery production and electrify our buildings, and VPP’s gain material volume, the economic incentives for distributed energy only grow.

Storage Forward

The speed of our transition to clean energy depends on our ability to replace gas generation with storage resources. While there are some headwinds: the net metering (NEM) 3.0 proposal demonstrated how vulnerable distributed energy could be to regulation, dispatch rules and tools must be built and refined, permitting and interconnection must be made easier, and the supply chain for batteries, including how they are procured and recycled needs to be resolved, an idea that was only worthy of a pilot just three years ago is now the operating assumption behind critical generation capacity in California. It is also the basis for a number of reference studies that demonstrate how the US achieves a 100% clean energy future without any leaps of faith.

We’ve seen that standalone and hybrid grid-attached deployments will ramp quickly because of their economic benefits, which only stand to improve with scale, while a combination of motivations may drive behind-the-meter storage growth. Regulators are making the rules for how these resources should participate in the energy ecosystem as we go along, and this to me is a good sign, and indicative of the undeniable value and appeal of the technology. It’s clear that storage has momentum. The economic advantage is there. The green benefit is there – energy storage is the capstone technology to eliminate the 25% of US CO2 emissions generated from energy production. We’re now firmly in the commercialization phase. No hype at all.

What are some points of leverage to accelerate storage?

1) Storage and hybrid systems' roles and treatment established and integrated in resource planning processes across regions.

2) Reducing interconnect queues through better grid analytics and proactive upgrades.

3) VPP/DER leaders emerge that can offer material economic benefit to distributed asset owners.

4) Accelerated permitting.

5) Grid analytics tools available to identify carbon emissions with more time- and location-based granularity.

6) Maturing of storage management software ecosystem to maximize storage revenue across multiple services.

7) Proving reliability value of storage in high demand and exceptional circumstances.

8) Strengthened carbon accounting and reporting requirements transition corporate focus from net-zero to 24/7 Carbon Free Energy (CFE).

9) EV share of new vehicle sales accelerate to scale battery production.

STORAGE TOPICS WE DIDN'T COVER

Long-duration storage (McKinsey)

Corporate PPA deals (Greenbiz) and new markets for 24/7 CFE

FURTHER READING

Lawrence Berkeley National Lab (LBNL) review of utility-scale solar in 2021 (LINK)

EIA on calculating economic value of generation, LCOE and LACE (LINK)

The Energy Transition Show (podcast) - Storage on the Grid (2015, LINK)

NREL study on how different storage systems can meet 100% renewable energy goals (LINK)

NREL study on 100% renewable Los Angeles (LINK)

Issues with today’s resource adequacy (capacity) planning practices (LINK)

Interested in hearing more? Subscribe and follow @greenwashalert